Long-term disability insurance protects a portion of your personal income if you become disabled, giving your family peace of mind. But what happens to your practice if you’re unable to work? Business overhead expense insurance can help keep your practice doors open and operating smoothly in your absence.

What is business overhead expense insurance?

We have a lot of practice-owning dentists, physicians and veterinarians ask, “Should I buy business overhead expense coverage? What does it actually cover, and do I really need it?”

Business overhead expense (BOE) insurance specifically addresses the ongoing costs of maintaining a small business when the owner is unable to work due to a disability. This includes reimbursements for fixed expenses such as rent or mortgage payments, utilities and other overhead costs critical to daily operations. It can also help to retain staff by ensuring continued compensation during a time of financial uncertainty.

What does business overhead expense insurance cover?

Practice owners should carefully review their business overhead expense insurance policy to understand what is and isn't covered, as coverage varies depending on the insurer and policy terms. However, here are some examples of common business expenses that a BOE policy might cover:

- Rent and lease payments: Includes payments made for the premises, equipment and furniture.

- Employee salaries, wages and benefit payments: Includes employment taxes for employees.

- Utilities: Includes phone, internet, electricity, water, heating, etc.

- Insurance premiums: Includes malpractice, property, liability and business insurance.

- Administrative expenses: Includes billing, accounting, legal and other similar business fees.

- Services: Includes laundry, janitorial and maintenance costs.

- Professional dues: Includes trade and association dues.

- Loan payments: The greater of depreciation or principal payments on business loans on business property.

- Interest on business debt: Applies to debt existing on the day your disability begins.

- Business property taxes: Includes taxes due on business-owned property.

That said, there are some operating expenses that aren’t typically covered. For example, although BOE insurance reimburses for employee wages, it won’t cover your own salary. That’s why personal disability insurance is necessary.

Here are some sample expenses that BOE insurance doesn’t generally cover:

- Bonus, incentive compensation, profit sharing and commission payments.

- Compensation to a family member who wasn’t employed by your practice at least 60 days prior to your disability.

- Cost of sales and inventory.

- Travel and entertainment expenses.

- Income taxes and excise taxes.

- Expenses for any capital equipment purchased after the date of disability.

To be clear, business overhead expense insurance only kicks in when the owner has a qualifying disability. It doesn’t apply to other business interruptions caused by natural disasters, economic downturns or other external circumstances.

When to consider BOE insurance for your practice

Business overhead expense insurance covers your practice’s routine expenses while you recover from a disabling injury or illness. Whether you need reimbursement for several months, a year or longer, BOE insurance is a must if your absence might jeopardize your practice, causing you to close or make changes that could have long-term consequences.

Let’s say you own a dental practice and have a small team of hygienists and administrative staff. As a solo practitioner, the business completely falls on your shoulders. So, not being able to work and earn income for your business for an extended period of time could have detrimental effects on your practice and staff.

As a medical, dental or veterinary practice owner, you’ll want to consider questions like:

- Are you set on keeping all of your employees during a period of financial instability? Or can you easily hire new staff after you recover?

- If you’re part of a group practice, can your partners manage temporarily without you by distributing the financial burden and additional workload? How do you plan to cover your share of the business expenses while you recover?

- What happens if you experience a permanent disability and, therefore, won’t be able to practice and function in the business going forward?

Business overhead expense insurance won’t replace you. But it can help prevent you from having to close your practice for an unknown amount of time — allowing you to preserve patient relationships and safeguard the value of your practice in case you have to sell at a later date.

Business overhead expense insurance: What to expect

Just like with an individual disability insurance policy, you’ll have a variety of policy decisions to tailor. For example, business overhead insurance coverage generally has a benefit period ranging from 12 to 24 months and an elimination period between 30 to 90 days. But unlike with long-term disability insurance, your maximum monthly benefit amount is based on your loss of net income and expenses.

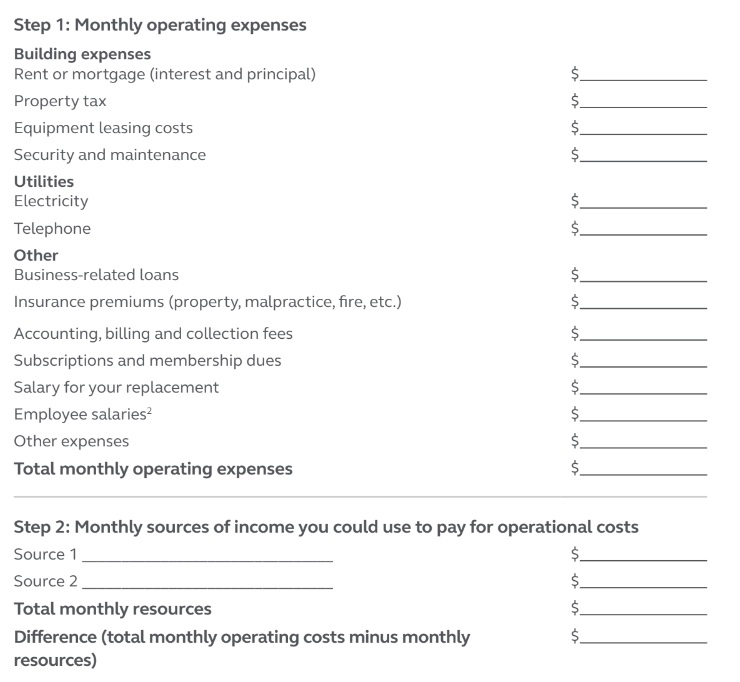

Here’s a sample worksheet to get a better idea of the business expenses that could be covered if you’re unable to work due to a disability:

Source: Principal Overhead Expense insurance

Note that BOE insurance allows you to roll over unused benefits to future months if your actual covered expenses are less than the policy’s monthly maximum benefit.

Additionally, the definition of disability will vary by policy. For example, overhead expense insurance with Principal defines disabled as being unable to perform the substantial and material duties of your occupation and:

- Have at least a 20% reduction in hours worked.

- Have a monthly loss of net income where expenses exceed monthly gross income by at least $200.

- Are under the care of a doctor.

Each insurance carrier also offers a variety of built-in features and optional riders. For example, The Standard offers a salary replacement rider that allows you to hire someone to perform your duties and have their salary included as a covered expense.

Other available add-ons might include residual disability benefits and a future purchase option rider that can be used as your practice grows and expenses increase.

How to get a business overhead expense insurance policy

Investing in both an individual disability policy and business overhead expense insurance can offer comprehensive protection against income loss and your share of business expenses, providing a more robust financial safety net.

Note that for group practice owners, a separate disability buy-sell policy can provide additional protection for the practice as it can help facilitate the purchase of a permanently disabled partner’s interest by the remaining partners.

To ensure you have the coverage you need for your family and your practice, fill out the form below to have SLP Insurance evaluate your existing individual coverage and overall need for business overhead expense insurance.

Compare disability insurance quotes and save

SLP Insurance will find you the best price on own occupation coverage, even if it's not with us. Fill out the form below for a quote with up to 30% discounts.

FAQ: Business overhead expense insurance

A business overhead expense policy typically reimburses for operational costs — such as rent, utilities, employee salaries, equipment leases and insurance premiums — if the business owner can’t work due to a disability.

Business overhead expense insurance doesn’t cover the owner's salary. Instead, it focuses on reimbursing essential business expenses while the owner is unable to work due to a disability.

Practice owners should maintain adequate individual disability insurance to ensure their personal income is protected in the event of an unexpected injury or illness.

Business overhead insurance premiums are tax-deductible as a necessary business expense.

Note the benefits you receive will be considered taxable income. However, your actual business expenses remain tax-deductible, so the net benefits are basically tax-free.