This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We experienced it all: studentloan debt, lack of affordable housing, mental health issues, child care challenges and underwhelming job prospects after graduation. It’s time to reframe the definition of legacy in higher education from a practice meant to exclude to one that’s inclusive of student-parents and their children.

“We should understand that affordability is one of the biggest challenges facing higher education, now and into the future, as evidenced by increasing studentloan debt,” said Dr. Linda Oubré, president of Whittier College in California. The total studentloan debt reached $1.75

According to the GAO report, students who pick a college that is unaffordable for them are more likely to have to cut back on essentials like food while attending and are more likely to drop out. Having more studentloan debt may make borrowers less likely to become homeowners or to be able to save for their own or their children’s futures.

An audience member asked about messaging around student debt cancellation. Russell responded, “Youth voters, I think seven in 10 support studentloan debt cancellation. I think there’s going to be a big fight coming this year with the courts, and something we are definitely watching and hoping to be a resource for.”

“We had quite a few students who deposited, who committed to us, but when they received their bills in July, they realized that Mason wasn’t affordable for them, even after taking out the max in studentloans,” said Byrd. “It It definitely made us realize that we need to make a significant investment in need-based aid.”

Fact: Many families are surprised to learn they qualify for grants, work-study, or low-interest loans, regardless of income level. You never know what might come of it – and if you dont, theres definitely no way youll receive aid! Whether or not you think youre going to qualify, its always worth submitting your application.

In November 2022, the Department of Education published final rules that will change regulations governing a variety of federal studentloan cancellation programs as well as how interest impacts studentloan burdens. The Department expanded its definition of when a school is “closed.”

But due to its limitations, such as having a strict definition of disability and capped benefits, employer-sponsored disability coverage usually isn’t enough to cover the needs of high-income earners. Get Supplemental Disability Insurance appeared first on StudentLoan Planner. Do you need supplemental disability insurance?

The exception to this rule is funding received as a result of a federally declared state of emergency—this is a broad category of federal assistance that helps people recover in the face of natural disasters, and part of its legal definition is that it is not considered taxable income. What about studentloan repayments and forgiveness?

Key Takeaways: Physicians need a strong definition of disability to protect their specialty income and education investment from an unexpected injury or illness. When searching […] The post Guardian Disability Insurance Review: Enhanced True Own-Occupation Coverage for Physicians appeared first on StudentLoan Planner.

There are many decisions physicians need to make when buying disability insurance, including choosing a strong definition of disability and deciding whether to include policy riders that will enhance your coverage. One rider to consider is a catastrophic disability benefit.

But the best disability insurance for physicians carries a true own-occupation definition of disability, with the strongest income protection for your medical or dental specialty.

For example, choosing an own-occupation definition of disability allows you to collect benefits based on your ability to perform […] The post Partial Disability vs. Total Disability: How a Partial Disability Rider Changes Your Coverage appeared first on StudentLoan Planner.

Policies have specific criteria for determining eligibility, and definitions for qualifying medical conditions can vary from policy to policy. Knowing what medical conditions […] The post Your Guide to Which Medical Conditions Qualify for Long-Term Disability appeared first on StudentLoan Planner.

Your education and specialty training need protection beyond the standard definition of disability. Read on to learn about long-term disability insurance for pulmonologists, including estimated costs, […] The post How to Buy Disability Insurance for Pulmonologists With The Strongest Protection appeared first on StudentLoan Planner.

As a high-income earner, you can receive a substantial payout if you can’t perform your specialty, depending on your policy’s definition of disability. appeared first on StudentLoan Planner. That said, you’re probably wondering, “How much disability insurance do I need?”

But you might be dangerously underinsured if your policy doesn’t have a true own-occupation definition. An own-occupation disability insurance policy pays you if you can’t work in your occupation […] The post Own-Occupation Disability Insurance: What It Is and Why You Need It appeared first on StudentLoan Planner.

To wrap up your financial aid journey, here’s a few things I recommend for the class of 2024… Make sure the FAFSA has your 2023 tax info: April 15 is almost here and you should definitely have completed your 2023 taxes by now. Review the differences between private and federal loans.

Get more information For more on recruiting adult student populations, including graduate students, subscribe to the Professional and Adult Education Blog. Who they are Typically, adult learners—sometimes called “non-traditional students,” although that definition is fading from the vernacular—are defined as students aged 25 or older.

When deciding on the type of savings plan, you should definitely talk to a financial advisor who can help find a plan that is best for your family’s needs. #2: 2: Teach your children more about the value of money this year Too many students reach college age without having any concept of the value of money. See them on the blog today!

COA: Changes are being made to the definition of Cost of Attendance. Some students with extremely low income may be able to qualify for financial aid which exceeds the cost of attendance. Untaxed Income: Changes have been implemented to streamline the definition of untaxed income and benefits.

From understanding federal and private studentloans to exploring alternative funding options, we’re here to help you navigate the world of finance for studying abroad and make informed decisions every step of the way. Key takeaways Understand federal and private studentloans to finance your study abroad experience.

Know when your college requires a definite commitment from you, and adhere strictly to that deadline. You’ll find information on everything including admissions deadlines, financial planning, filling out the FAFSA, award letters, searching for scholarships, and comparing studentloan options. Still Want More Help?

This will definitely vary between colleges and states. More about Jodi and College Financial Aid Advisors Jodi is a FAFSA financial advisor who helps with the financial aid process to help families of college students maximize their financial aid. Check out those tips here!

Differences between scholarships and studentloans. Scholarships and studentloans are two ways to finance your education. Studentloans, on the other hand, do need to be repaid, but you can usually take out enough to cover the entire cost of your education. Who can apply for scholarships?

will definitely result in big celebrations. More about Jodi and College Financial Aid Advisors Jodi is a FAFSA financial advisor who helps with the financial aid process to help families of college students maximize their financial aid. High school seniors are determining where they’re going to school and how to pay.

The bottom line is that if you don’t file the FAFSA, you definitely won’t receive any aid for school. A common misconception is that based on a family’s life and finances, their student won’t receive aid. Additionally, many states and colleges use the FAFSA to determine eligibility for their own financial aid programs.

My team has worked with an increasing number of institutions that are seeking to re-center their student success strategies around a more holistic definition of the student experience. This summer, my friends on EAB's enrollment research team surveyed over 20,000 high school students to gather insight into recruiting Gen P.

as an international student can be challenging, but there are resources available to help. Private studentloans are an option for those who need to cover tuition costs but may not qualify for federal financial aid. as an international student is definitely possible.

Black students still face obstacles in schools, such as still having a higher likelihood to have uncertified teachers (4.9%) and inexperienced teachers (15.2%) compared to their white peers (2.1% And you can definitely see that, where Black students continue to be underrepresented in gifted and talented education by 50 to 55%.”

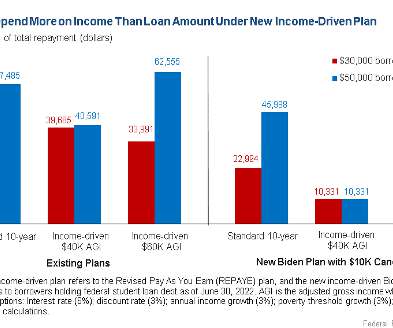

Although the news cycle has been dominated by the Biden administration’s studentloan forgiveness program and its fate at the U.S. With IDR plans, studentloan recipients’ monthly payments are based on their incomes, instead of being set at a fixed amount.

Title III of the legislation contains the Committee on Education and Workforce’s proposed changes to the Department of Education’s (ED) student aid programs, including Pell Grants, studentloans, and the aid eligibility formula. 1 was designed to rectify the government’s convoluted studentloan system and save $351 billion.

Department of Educations efforts to reduce studentloan burdens through the new SAVE repayment plan. As a result, borrowers options to manage their loans have changed repeatedly and often quite suddenly. This has been frustrating and confusing for people trying to manage their loans.

Department of Educations efforts to reduce studentloan burdens through the new SAVE repayment plan. In Part 2, we break down exactly what the recent court orders mean for studentloan borrowers. For what this means for borrowers, see Part 2 here. These lawsuits are ongoing; there are no financial decisions yet.

Our discretionary income calculator below (fully updated with the latest 2023 poverty line numbers) will show you the brand new definition of discretionary income for 2023 when studentloan payments start again. The post Discretionary Income Calculator for the New IDR Plan in 2023 appeared first on StudentLoan Planner.

.” (COE is working with the Administration to gain additional insight into this latter portion of the request and will share details with the community as soon as they become available.) Increase for TRIO for FY 2023 Advocacy Update Congress Announces Bipartisan Funding Deal, Includes 4.7%

Studentloan balances have spiked in the last few years. To reduce this burden, President Biden announced the StudentLoan Forgiveness Plan (the Plan) in August 2022. It forgives $10,000 of student debt for borrowers earning less than $125,000 per year, and up to $20,000 for former Pell Grant recipients.

Since 2021, the Biden administration has forgiven $138 billion in studentloans for 3.9 The Administration announced on February 21 that another category of borrowers would have their loans forgiven by the end of the month. million borrowers.

The studentloan landscape has changed dramatically, thanks to the government’s August announcement of up to $20,000 in loan forgiveness. Specifically, those who received a Pell grant during college can qualify to have up to $20,000 of their current federal studentloan balance canceled. Note: As of Nov.

The studentloan debt crisis has been out of control for a long time. So, if you are one of the 42 million Americans who have studentloan debt, you’re understandably watching what President Biden is doing to address this issue. . Should you keep making payments on your studentloans? .

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content